|

by

Courtenay Turner

May 19, 2026

from

CourtenayTurner Website

|

My co-author and I will continue

to hammer on tokenization because it is the monster

on the loose, the clear and present danger.

It is

redefining ownership from the bottom up.

Your

"sovereign property" will be subverted and turned

into "user rights" where "you will own nothing."

In

reality, Tokenization of all assets is the biggest

heist in the history of the world.

Source |

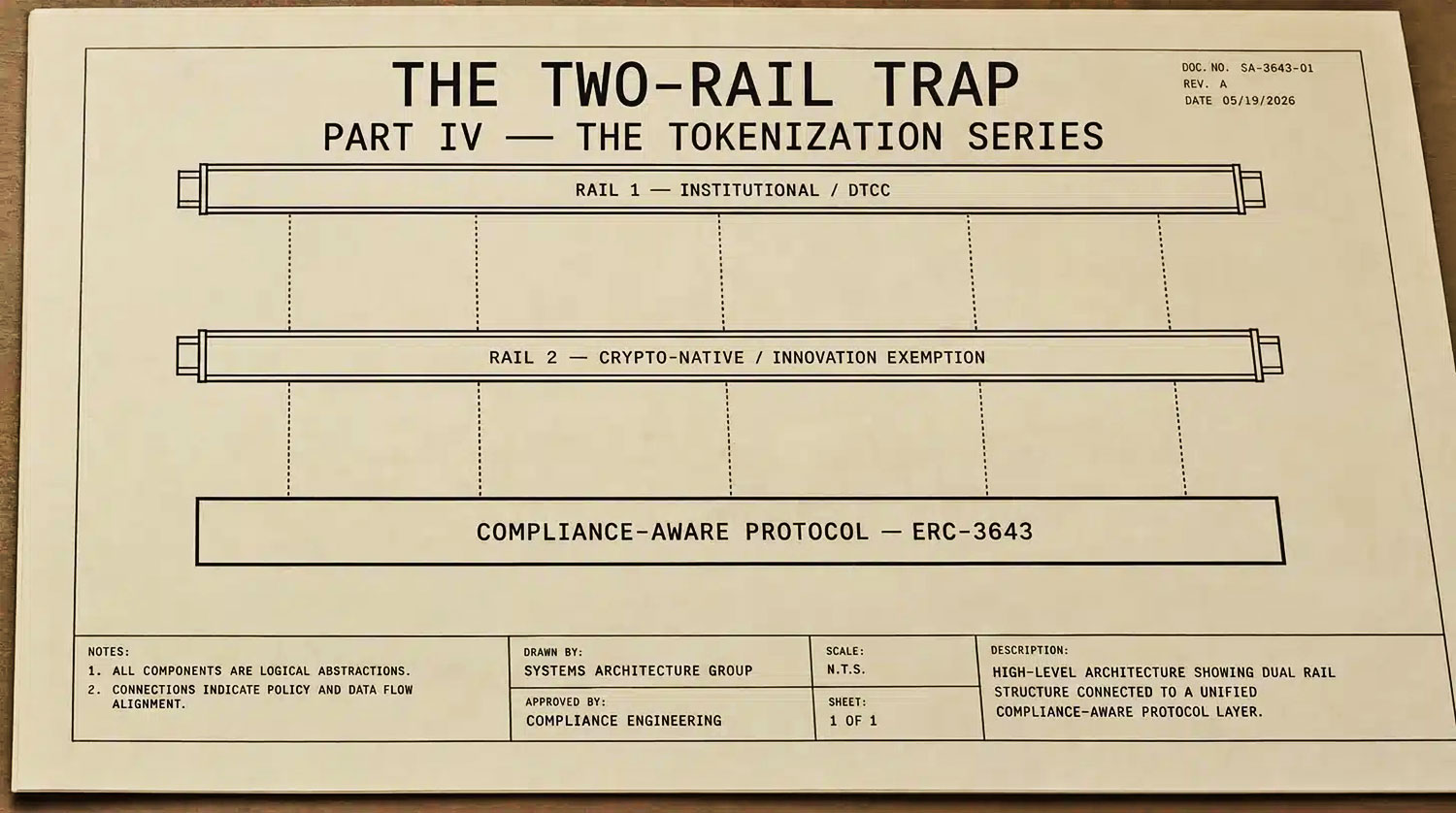

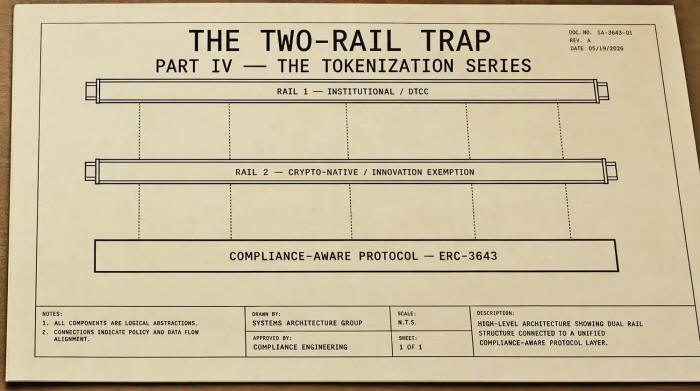

The SEC is about to authorize

a second, parallel path

for putting

U.S. equities on-chain

- one that does not have

to be the equity at

all.

Read alongside the DTCC rollout,

this is not a competition

between models.

It is a pincer...

The Move the Market Refused to

Hear

In Part I,

The Tokenization of Everything, I described the asset

layer:

programmable digital instruments inside a regulated,

bank-integrated ecosystem, where ownership quietly mutates into

conditional permission.

In Part II,

The Proof of Persona, I described the persona layer:

identity, eligibility, attention, and eventually body-derived

signals rendered into ledger-native attestations.

In Part III,

The Tokenization Chokepoint, I documented what the DTCC

announced on May 4, 2026 - the rollout of the institutional asset

layer, scheduled for July production trades and an October launch,

with fifty of the world's largest financial firms in the working

group.

The

DTCC rail was, I argued, the institutional

half of the architecture:

the same legal entitlement, wrapped in a

programmable, freezable, force-transferable, sanctions-screened

compliance envelope.

"Same rights, same protections, same

entitlements" on paper.

Programmable, reversible, permissioned by

design in the actual code.

I closed Part III by saying the rollout begins in

July, the architecture is not yet closed, and the argument cannot

wait.

Two weeks later, the other shoe dropped.

On May 19, 2026, Forbes published Zennon Kapron's

piece, America

is About to

Have Two Stock Markets for the Same Company.

Bloomberg had

reported the day before that the SEC's "innovation exemption" for

tokenized stocks could land within the week.

The agency, under Chair

Paul Atkins' "Project Crypto," is preparing to bless a

second path for putting U.S. equities on-chain - and the

second path is not the same product as the first.

The institutional rail captures the spine of U.S.

capital markets through DTCC. The crypto-native rail captures

retail, offshore, and 24/7 price discovery through Robinhood,

Kraken, Bybit, Backed, xStocks, BNB Chain, and the rest. Together,

the two rails do not compete. They enclose.

This is Part IV.

This is the pincer...!

What the

Innovation Exemption Actually Does

Atkins did not hide what he was building.

In his July 31, 2025

speech at the America First Policy Institute - formally titled

American Leadership in the Digital Finance Revolution - he told the

audience that,

"firms - from household names on Wall Street to

unicorn tech companies in Silicon Valley - are lined up at our doors

with requests to tokenize," and that the SEC would "provide relief

where appropriate to assure that Americans are not left behind."

He

laid out the design of the exemption in the same speech: periodic

reports to the Commission, whitelisting or verified-pool

functionality, and adherence to a "token standard that incorporates

compliance features, such as ERC-3643."

ERC-3643 was the only token standard Atkins cited by name in the

speech.

That detail matters, because it is the same ERC-3643 that DTC explicitly names in its request letter to the SEC's Division of

Trading and Markets as a "compliance aware" protocol satisfying the

requirements for "distribution control" and "transaction

reversibility."

It is the same token standard at the core of the DTCC architecture I described in Part III.

DTCC is itself a member

of the ERC-3643 Association governance body. Both rails - the Wall

Street rail and the crypto-native rail - are not merely converging

on the same permissioned, reversible, OFAC-screenable token

primitive in the abstract. They are converging on the same named

standard, with the same compliance-aware affordances, with the same

governance association in the background.

That is not coincidence. That is interface standardization.

Different chains, different protocols at the edges, but the same

compliance grammar at the center.

The crypto-native rail also has its own legal scaffolding.

On

January 28, 2026, the SEC's Divisions of Corporation Finance,

Investment Management, and Trading and Markets jointly published a

staff statement dividing tokenized securities into two categories:

those tokenized by or on behalf of the issuer, and those tokenized

by third parties unaffiliated with the issuer.

The staff further

specified that third-party wrappers come in two sub-flavors -

custodial wrappers (where the issuer of the token holds the

underlying security in custody and the token represents a claim

against the custodian) and synthetic wrappers (where the token

tracks the price of the underlying without holding it at all).

For

the third-party category, the staff wrote that the rights and

benefits associated with the crypto asset,

"may or may not be

materially different from those of the underlying security" and "may

or may not confer upon the holder of the crypto asset any rights as

a holder of the underlying security."

Read that sentence twice.

The SEC is preparing to bless a market in things that look like

Apple stock, trade against the price of Apple stock, and do not have

to be Apple stock.

Things that may carry voting rights, or may not.

Things that may represent ownership, or may not.

Things that may be

security-based swaps, linked securities, or tokenized security

entitlements - three different legal animals as defined by the SEC's

own staff - depending on which wrapper the issuer (or the third

party) chose to mint.

Brett Redfearn, the former SEC Division of Trading and Markets

director who now runs the tokenization firm Securitize, put the

consequence plainly in the Forbes piece.

If third parties can

tokenize Apple or Amazon without the issuer at the table, there is

no theoretical limit on how many wrappers of the same company exist

at once. Multiple parallel wrappers means investors are uncertain

what their shares are worth at any given moment, and price discovery

has no single canonical reference.

That is not a Reg NMS purist

talking. That is a critique from inside the tokenization industry.

"Same Rights" Was Always Only Half

the Architecture

In Part III, I tried to be precise about the DTCC rail.

The

institutional reassurance - same legal entitlement, same Article 8

protections, same dividends, same voting rights - is real on its own

terms. The SEC's December 11, 2025 no-action letter was explicit

about it. The legal wrapper preserves the entitlement.

What I argued was that the technical wrapper introduced an entirely

new control surface beneath the legal wrapper. Both are true at

once. That was the point.

The innovation exemption now closes the other half of the loop.

Where the DTCC rail tells you that the legal entitlement survives

tokenization in full, the crypto-native rail tells you, in the SEC

staff's own words, that the legal entitlement may or may not survive

at all.

Two onshore market structures for the same equity, with two

completely different relationships to ownership.

Here is what this looks like in practice, once both rails are

running:

Rail one (DTCC):

Your equity exists as a token in a Registered

Wallet on an approved chain, under a compliance-aware protocol,

subject to root-wallet override and LedgerScan surveillance.

The

legal entitlement is preserved. The exercise of it depends entirely

on the system's recognition of your wallet, your protocol, and your

standing. Programmable compliance with full legal rights.

Rail two (the innovation exemption):

Your equity exists as a token

on a crypto-native platform, possibly minted by a third party who

has no relationship to the issuer, possibly conferring no

shareholder rights at all, possibly classified as a security-based

swap, a synthetic linked security, or a tokenized security

entitlement - three different legal animals - depending on the

wrapper.

Programmable compliance with optional legal rights.

Both rails are permissioned. Both rails are reversible. Both rails

are surveilled. Both rails are sanctions-screenable. Both rails are

built on the same compliance-aware protocol standards.

The only difference is how much of the underlying ownership claim

makes it through the wrapper.

That is not two stock markets for the same company.

That is two

cages for the same equity, sized for two different captives.

Two cages for the same equity.

Rail One preserves the entitlement

inside a programmable envelope.

Rail Two dispenses with the

entitlement and offers price exposure instead.

Why the Pincer Works

The two-rail architecture is what makes the rollout structurally

complete, and it is why it should be read as a single design choice

rather than two separate ones.

The institutional rail captures the bulk of regulated capital -

pensions, retirement accounts, mutual funds, sovereign wealth, bank

treasury books - by preserving "same rights, same protections."

It

is conservative-by-design because the constituency that holds $114

trillion through DTC is not going to migrate into a platform that

strips voting rights and dividend entitlements. They need the legal

wrapper to remain intact, and DTCC delivers it. Slow, walled,

regulated, programmable.

The crypto-native rail captures everything the institutional rail

leaves on the table. Retail traders who want 24/7 settlement.

Offshore capital that already migrated to xStocks, Backed, Kraken,

Bybit, Robinhood EU, BNB Chain.

Yield-chasing flows that want

fractionalization, automated market makers, and frictionless

cross-platform liquidity. People who do not care whether their

"Apple token" actually represents Apple stock as long as it tracks

the price. Fast, open, light-touch, programmable.

Mark Greenberg, Kraken's global head of consumer, told DL News in

September that,

"the future of capital markets will not be one-size

fits all" and that "the real technological breakthrough lies in permissionless, interoperable platforms like xStocks."

Translate

that. Kraken's pitch is that an Apple token trading 24/7 with no

settlement friction will pull volume away from an Apple share that

clears T+1 through NSCC, regardless of whether the holder of the

open-rail token actually owns the underlying.

Price discovery, not

legal ownership, is the value proposition.

That is the exact inversion I named in Part I. Possession becomes a

system-recognized entitlement. The legal claim is decoupled from the

trading venue. The economic exposure is decoupled from the rights of

the shareholder.

And once the crypto-native rail captures price

discovery - once the Apple token on Solana or Canton or BNB Chain

becomes the most liquid venue for trading Apple - the DTCC rail and

the issuer's transfer agent become a back-office formality. The

"real" market is wherever the price moves.

ESMA, the European securities regulator, has publicly warned that

tokenized equity wrappers carry a "risk of misunderstanding" for

retail investors who may not realize their tokens do not confer

shareholder rights.

That warning has been issued in Europe, where

the wrappers are already live. It is about to land harder once the

same wrappers are available onshore in the United States - with the SEC's blessing - and once the legal-rights gradient between rail one

and rail two becomes invisible to anyone who is not a securities

lawyer.

This is the operational form of the subscription society I described

in Part I. The cage is not built by coercion. It is built by

dependency, by gradient, by convenience, and by the quiet retirement

of the alternative. The DTCC rail is the dependency. The

crypto-native rail is the convenience.

The alternative - a

non-programmable, non-tokenized, name-on-the-books equity holding -

is the thing being quietly retired.

The CLARITY Act Is the Legislative

Half of the Two-Rail Design

The administrative half of the architecture is what I have been

documenting - the December 2025 DTC no-action letter, the January

28, 2026 joint staff statement, the imminent innovation exemption.

The administrative half can move fast because it does not require

Congress to do anything.

Staff discretion, Commission letters,

principles-based safeguards, three-year pilots - the entire

vocabulary of Project Crypto is designed to construct durable

infrastructure under the umbrella of "we're just clarifying existing

law."

The legislative half is the CLARITY Act.

I named CLARITY in Part I as part of the legislative scaffolding for

tokenization, alongside the GENIUS Act. I have not yet given it the

structural treatment it deserves in this series, because until the

innovation exemption surfaced this week, the question of how the two

halves interlock was still partly speculative.

It is no longer

speculative. The two halves are interlocking in public, in front of

the same Congress that voted GENIUS through last year, on the same

timeline as the rollout I documented in Part III.

The Digital Asset Market Clarity Act - H.R. 3633 in the 119th

Congress - passed the House in 2025. The Senate Agriculture

Committee marked it up in January 2026.

On May 14, 2026 - five days

before the Forbes piece that opened this essay - the Senate Banking

Committee advanced the bill in a 15-9 bipartisan vote, with all

thirteen Republicans joined by Democrats Ruben Gallego and Angela

Alsobrooks, both of whom stated that their support was conditional

and might not translate to floor votes.

The same day, Senator Chris

Van Hollen - co-author of the April 27 letter to Atkins about the

innovation exemption - saw his ethics amendment, which would have

barred senior government officials from holding certain crypto

business interests, defeated 11-13 in committee.

The bill now heads

to the full Senate floor, where it needs 60 votes to overcome a

filibuster. The Banking and Agriculture versions will also have to

be reconciled before a final floor vote.

The practical deadline is

August 2026, before midterm campaigning closes the legislative

calendar.

As of mid-May 2026, Polymarket has been trading the

"Clarity Act signed into law in 2026" market in the 65-75% range,

with the probability spiking around the Senate Banking markup; a

White House adviser publicly floated July 4 as a possible signing

target.

What CLARITY does, structurally, is sort every digital asset into

one of three regulatory boxes:

-

Digital commodities (Bitcoin, Ether, Solana, and tokens whose

networks are deemed "mature" or sufficiently decentralized) go to

the CFTC for spot and cash-market oversight.

-

Investment contract assets (tokens sold like an early-stage equity

round, where a centralized team raises capital against future

deliverables) stay with the SEC under the existing securities

framework.

-

Stablecoins (dollar-pegged tokens used to move money) get joint SEC/CFTC

oversight, building on the GENIUS Act's licensing regime.

Read that taxonomy against the SEC staff's two-category framework

for tokenized securities - issuer-tokenized vs.

third-party-tokenized, with third-party in custodial and synthetic

sub-forms - and the architectural fit becomes obvious.

Issuer-tokenized equities (the DTCC rail, with full Article 8

entitlement preservation) are unambiguously securities. They stay

with the SEC. The administrative architecture I documented in Part

III governs them.

Third-party custodial wrappers - where a platform like Backed or

xStocks holds the underlying security in custody and mints a token

that represents a claim against the custodian - sit at the seam.

The

SEC staff statement frames them as still securities, but the token

holder's rights run against the intermediary, not the issuer.

Under

CLARITY, the classification depends on whether the wrapping platform

is treated as the issuer of an investment contract asset (SEC) or as

a venue for a digital commodity (CFTC).

Third-party synthetic wrappers - tokens that track the price of

Apple stock without actually holding any Apple stock - are where the

architecture gets murkiest, and where I want to mark the line

between what the statute says and what I am projecting.

The CLARITY

Act's commodity classification is, on its face, about whether the

underlying network is sufficiently decentralized or "mature," not

about whether a particular wrapper confers shareholder rights.

A

synthetic equity-tracker might already be a security-based swap

under existing Dodd-Frank rules, which would keep it within SEC

jurisdiction regardless of how CLARITY's three-box taxonomy is read.

So the cleanest legal reading is that synthetic wrappers stay with

the SEC.

What I am interpreting, and want to be explicit about: my argument

is not that CLARITY's text directly reclassifies synthetic wrappers

as CFTC commodities.

My argument is that the combination of CLARITY's broad commodity-classification expansion, the SEC staff's

January 28 framing of third-party wrappers as instruments whose

rights "may or may not confer" anything against the issuer, and the

innovation exemption's lighter-touch treatment of crypto-native

platforms creates an interpretive gradient.

Wrappers that confer

full shareholder rights stay unambiguously with the SEC.

Wrappers

that confer no rights, that resemble price-tracking commodities more

than equity claims, and that trade on crypto-native venues styled as

digital-commodity infrastructure are the most contested ground in

the federal jurisdiction map - and the gravitational pull of CLARITY's CFTC expansion, combined with Project Crypto's posture

toward lighter-touch oversight, is toward the CFTC end of that

gradient.

That is interpretation, not statutory text. But it is the

interpretation the design choices invite. The legal-rights gradient

I described in the previous section is not just a market-structure

gradient. It is - at least at the boundary cases - a regulator

gradient.

That is not an accidental drafting outcome. That is the design.

It is also the design that NASAA - the North American Securities

Administrators Association, representing state securities regulators

across all 50 states, D.C., the territories, and Canadian and

Mexican jurisdictions - flagged formally in a January 13, 2026

comment letter to Senate Banking Chair Tim Scott and Ranking Member

Elizabeth Warren.

NASAA wrote that it was "unable to support the

CLARITY Act in its current form" because "provisions contained in

Title I will weaken existing state authority to combat investor harm

stemming from cases of fraud and abuse in digital assets

transactions."

The letter identified "fundamental internal

inconsistencies" in the bill's definitions - particularly the

unworkable separation between "network token" (a digital commodity

under the CLARITY Act) and "ancillary asset" (a network-token

subcategory whose value depends on entrepreneurial or managerial

efforts of others, a Howey-test condition). NASAA warned plainly:

"Fraudsters will exploit any new conditions and limits to these

concepts. Given the epidemic of fraud being perpetrated against

American investors, especially older investors, Congress should not

pursue policies that will make it easier for scam artists to get

away with their crimes and harder for law enforcement and regulators

to act."

This is a slightly different concern than the Warren/Van Hollen letter on the innovation exemption - NASAA's focus is on

state anti-fraud authority and the preservation of the

investment-contract definition under NSMIA, where Warren/Van Hollen

targeted the federal exemption pathway - but it lands on the same

structural worry: market participants drifting outside the

protections of the securities laws through definitional architecture

rather than substantive change.

The state regulators and the Senate

Democrats are flagging the same architectural risk from two

different directions. Neither alone is sufficient to stop the

architecture.

Together, they constitute the institutional skeleton

of an opposition that does not yet exist as a coalition.

The GENIUS Act gave Atkins the stablecoin rail.

The CLARITY Act

would give him the commodity rail and seal the SEC/CFTC

jurisdictional reallocation against future Commission turnover. The

innovation exemption is the proof-of-concept; CLARITY would be the

durable statutory backing that prevents a future Democratic SEC from

rolling it back.

That is why the timing matters. Atkins' term as

Chair expires June 2026. CLARITY's window to clear the Senate

effectively closes in August 2026. Both deadlines fall before the

November midterms.

This is what I meant in Part I when I called GENIUS and CLARITY the

iron scaffolding of a technocratic system. The bills are the rails.

The no-action letter and the innovation exemption are the trains.

ERC-3643 is the gauge. And the constituency that designed the

architecture is racing to lay all three before the political

composition that authorized it changes.

The legislative half also clarifies what is, and is not, fixable

through public comment on an SEC release. The innovation exemption

can be modified or revoked by a future Commission.

CLARITY, once

signed, cannot. The two halves of the design are doing different

things on different timelines, and the legislative half is the

harder one to undo.

Reg NMS Is Not Collateral Damage - It Is the Target

The slower-moving consequence of the innovation exemption, Kapron

notes, is a rewrite of the rules that built the modern U.S. equity

market structure. National Market System protections - best

execution, the consolidated tape, the principle that one stock has

one canonical market - were built on the premise that a regulated

trading venue is the architecture worth defending.

Atkins

co-authored the original dissent to Reg NMS in 2005 and said in his

July 2025 speech that accommodating tokenized trading "may require

us to explore amendments to Reg NMS."

He said it in public. The market chose not to hear it.

The Forbes piece treats the dismantling of Reg NMS as a

market-structure cost - fragmentation, price-discovery uncertainty,

settlement-mechanic divergence. I read it differently, and I think

the design choice reads more clearly through the frame I have been

using across this series:

a single canonical market for each equity

is exactly what you have to dissolve in order to make the

programmable, permissioned, surveilled rail durable.

If one stock has one canonical market, then the canonical market is

the gravitational center of price discovery, shareholder activism,

transfer-agent accountability, and Reg NMS surveillance. The

legal-rights wrapper and the trading-venue wrapper are the same

wrapper. The issuer has somewhere to sue. The shareholder has

somewhere to vote. The regulator has somewhere to look.

If a stock has many wrappers - some preserving rights, some not,

some on crypto-native chains, some on permissioned institutional

ledgers, some custodied, some synthetic, some swaps, some

entitlements - then there is no canonical market. There is a swarm

of correlated venues, and the question of which one is "real"

becomes a function of liquidity rather than law.

One equity, many wrappers,

no canonical market.

The fragmentation is

not a bug,

it is the design choice.

In that environment, the role of the regulator subtly shifts.

The

SEC stops policing a market and starts certifying protocols. The DTC

stops being a depository for shares and starts being a custodian for

tokenized entitlements.

The exchanges stop competing on execution

quality and start competing on settlement speed and credential

schemas. And every one of these venues - institutional and

crypto-native alike - runs on compliance-aware token standards with

root-wallet authority, reversibility, surveillance, and OFAC

screening baked into the protocol.

The political question is no longer "where can you trade Apple." It

is "whose compliance envelope are you trading inside."

Once that

becomes the question, sovereignty over capital allocation has

migrated out of the regulated exchange and into the protocol

designers, the compliance-aware standard-setters, and the

institutions that operate the root wallets.

This is what I meant in Part I when I wrote that decision-making

shifts from democratic processes to elites and code. The innovation

exemption is the part of the architecture where the code starts

writing the law.

Where Loop 2 Plugs In

In Part III I argued that the DTCC rail completes Loop 1 - the asset

layer - and lays the rail for Loop 2, the persona layer. The

credential gate today is institutional: a wallet is Registered

because a DTC Participant vouches for it under existing KYC/AML

obligations.

The short logical step is from "verified by KYC" to

"verified by attestations of identity, residency, accreditation,

sanctions standing, and tax status" to "verified by ledger-native,

soulbound, or body-derived attestations satisfying the system's

eligibility schema."

The innovation exemption accelerates this rail-laying, because it

brings the same credential question to the crypto-native rail under

explicit SEC blessing. Atkins' July 2025 design language - "whitelisting

or verified-pool functionality" - is the persona layer in regulatory

English.

The crypto-native rail is not, as its evangelists pitch it,

a permissionless system. It is a permissioned system whose

permissioning gate is the verified pool, the white-listed

buyer/seller, the compliance-aware token standard with distribution

control.

The same vocabulary as the DTCC rail. The same affordances.

The same trajectory.

Once both rails are live, the question of which attestations a

wallet must satisfy to participate in either rail becomes the entire

game.

It is the same question I posed in Part II, now embedded in

the official equity market on both sides:

"This wallet is verified because the holder has presented identity,

residency, accreditation, sanctions standing, and tax attestations."

→

"This wallet is verified because the holder has presented

ledger-native, soulbound, or body-derived attestations satisfying

the system's eligibility schema."

I am not claiming that integration is happening today. I am

claiming, again, that the rail is now built such that it can.

The DTCC rail laid one half of the asset-layer architecture in May. The

innovation exemption is about to lay the other half. Between them,

every public-company equity in the Russell 1000 will have a

programmable, permissioned, surveilled representation onshore - and

the credential layer that decides who is eligible to touch it is the

obvious next interface to standardize.

Layer 1 controls the asset. Layer 2 decides who is eligible to touch

it. Both rails of Layer 1 are now scheduled. Layer 2 has somewhere

to plug in.

What This Does Not Prove

Because the temptation in this terrain is to overshoot, let me be

explicit, as I was in Part III, about the boundary between evidence,

interpretation, and projection.

What the evidence shows:

-

The SEC's January 28, 2026 joint staff statement (Corporation

Finance, Investment Management, and Trading and Markets) defining

two categories of tokenized securities, with the second (third-party

wrappers, in both custodial and synthetic sub-forms) explicitly

framed as "may or may not" confer shareholder rights.

-

Bloomberg's May 18, 2026 reporting - surfaced in CoinDesk,

Unchained, PYMNTS, and elsewhere - that an innovation exemption for

tokenized stocks under Chair Atkins' Project Crypto could land

within the week.

-

Atkins' July 31, 2025 speech at the America First Policy Institute,

American Leadership in the Digital Finance Revolution, laying out

the design of the exemption: periodic reports, whitelisting or

verified-pool functionality, and adherence to "a token standard that

incorporates compliance features, such as ERC-3643" - the only token

standard named in the speech, and the same standard DTC names in its

request letter to the SEC's Division of Trading and Markets.

-

DTCC's membership in the ERC-3643 Association governance body,

confirming that the institutional rail and the named crypto-native

compliance standard share an organizational backbone, not merely a

technical one.

-

Atkins and Commissioner Peirce's February 2026 sketch of a temporary

framework that would include volume caps, white-listed buyers and

sellers, and automated market makers operating under

principles-based safeguards.

-

Atkins' explicit statement that accommodating tokenized trading "may

require us to explore amendments to Reg NMS."

-

The documented growth of the offshore tokenized-stock model: from

under $30M aggregate market cap at the start of 2025 to roughly

$1.2B by year-end, with xStocks alone surpassing $25B in cumulative

transaction volume across that period.

-

The April 27, 2026 letter from Senators Warren and Van Hollen

demanding an answer on whether further exemptions would "allow

market participants to easily escape the securities laws using

crypto," with a May 8 deadline that the Commission answered by

signaling this week's release.

-

The fact that OpenAI and Anthropic have already publicly disavowed

unauthorized tokenized products linked to their valuations on

offshore platforms - establishing the precedent that named,

large-cap issuers will, in fact, push back when their equity is

wrapped without consent.

-

The CLARITY Act (H.R. 3633) passing the House in 2025, Senate

Agriculture Committee marking it up in January 2026, and Senate

Banking Committee advancing it 15-9 on May 14, 2026 (with Van

Hollen's ethics amendment defeated 11-13 the same day), heading next

to a full Senate floor vote requiring 60 votes to overcome a

filibuster, with a practical August 2026 ceiling.

-

NASAA's January 13, 2026 comment letter formally opposing the

CLARITY Act in its current form on the grounds that Title I "will

weaken existing state authority to combat investor harm" and that

the bill's definitional inconsistencies between "network token" and

"ancillary asset" will allow fraudsters to "exploit any new

conditions and limits to these concepts."

What the evidence does not prove:

-

That every U.S. equity will be tokenized on the crypto-native rail.

-

That third-party wrappers will dominate price discovery for Russell

1000 names.

-

That the innovation exemption is being designed in explicit

coordination with the DTCC rail. (The architectural convergence on

ERC-3643 and compliance-aware standards is documented; the

coordination is inferred from the convergence.)

-

That any individual platform - Kraken, Robinhood, Bybit, Backed,

xStocks - is pursuing the architectural extensions I have described.

What I am interpreting:

-

That the DTCC rail and the innovation exemption rail, read together,

constitute a single architectural design choice: programmable,

permissioned, compliance-aware tokenization of U.S. equities across

both institutional and retail-facing venues.

-

That the deliberate fragmentation of legal-rights wrappers

(entitlement-preserving on the DTCC rail; "may or may not" on the

crypto-native rail) is the structural mechanism by which Reg NMS

protections become unenforceable and price discovery migrates to

whichever venue offers the most convenience.

-

That "innovation" - in this design - means a permissioned blockchain

wrapper that bypasses traditional broker-dealer registration, while

preserving the institution's ability to whitelist, reverse, freeze,

and screen at the protocol level.

That is enough to warrant scrutiny. It does not require maximalist

claims to be alarming.

The Polite Language of Enclosure,

Reprise

The rollout will not be sold as enclosure. It will be sold as

investor choice.

Investor choice between two rails. Investor choice between a 24/7

token wrapper and a T+1 settled share. Investor choice between a

fractionalized synthetic and a custodied entitlement. Investor

choice between a crypto-native AMM and a Nasdaq order book. Investor

choice between a token that confers shareholder rights and one that

does not.

This is the same rhetorical pattern I named in Part III. Control

systems that offer no convenience are easy to refuse. Control

systems that offer menu items - pick your rail, pick your wrapper,

pick your settlement speed, pick your compliance gradient - are

adopted voluntarily until opting out becomes impractical. Then the

menu becomes the market. Then the menu becomes the only place

ordinary participation in equity markets, retirement accounts,

brokerage relationships, and 401(k) plans is possible. Then the

question of whether you "consent" to programmable, freezable,

reversible, root-wallet-overridable ownership - or to a third-party

wrapper that may not confer ownership at all - becomes academic,

because the unprogrammed alternative has been quietly retired.

The innovation exemption is the menu expansion. The DTCC rollout is

the kitchen. The compliance-aware protocol is the recipe. Across

both rails, the meal is the same.

And the slowest, most defensible version of the cage - the one I

named in Part I, deepened in Part II, documented in Part III, and

now see operationalized through both the institutional and

crypto-native rails simultaneously - is the cage built by

dependency, by gradient, and by the polite withdrawal of any

non-programmable alternative.

The architecture does not refute the imago Dei.

It routes around it.

Personhood becomes an attestation.

Property becomes an entry.

Standing becomes a permission.

The Question Hiding Inside the

Technical One, Reprise

Beneath the engineering of the two rails is the same political

question I named in Part II, and beneath the political question is

the same metaphysical one.

Do persons exist prior to the system, or are persons constituted by

it? Does property precede the ledger, or does the ledger confer

property? Are rights inherent in the human person, or are they

permissions issued by a validation regime that decides which

wallets, which credentials, and which signatures qualify?

The DTCC rail answers that question one way: the legal entitlement

survives, but its exercise becomes contingent on the system's

recognition. The innovation exemption answers it more aggressively:

the legal entitlement may not survive at all, and the holder of the

token may have nothing more than a synthetic price-tracking

instrument with no rights against the issuer of the underlying

equity.

Both answers operationalize the same metaphysical premise. Ownership

is what the ledger says it is. Standing is what the protocol can

certify. Rights are what the verified pool admits. The Declaration

of Independence's premise - that persons are real prior to systems,

that dignity is intrinsic, that rights are not granted by the state

- is not refuted in either rail. It is simply rendered

unintelligible by the architecture. The system does not have to

argue against inherent rights. It has to make the question of

inherent rights non-actionable inside the only venues where capital

flows.

That is the deeper move I have been tracking across this series. The

Creator–creation distinction, the imago Dei claim, the realist

metaphysics that grounds the Declaration's argument - these are not

being attacked directly. They are being routed around, by an

architecture that treats personhood as an attestation, property as

an entry, and standing as a permission.

The two-rail design is what makes that routing complete. The

institutional rail preserves legal rights inside a programmable

envelope. The crypto-native rail dispenses with legal rights

altogether and offers price exposure instead. Together, they answer

the question of what a person is by not asking it - by making the

question irrelevant to the venues where ordinary financial life

occurs.

The Architecture Is Still Open. The Leverage Has Shifted.

The leverage points I named in Part III remain. They are now joined

by new ones specific to the innovation exemption.

The exemption itself is administrative. Like the December 2025 DTC

no-action letter, the innovation exemption is not statute. It is

staff and Commission discretion, granted under defined

representations, subject to modification or revocation. Public

comment to the Commission's public comment channels is the most

direct lever there is. As I noted in Part III, the SEC has only

three sitting commissioners - Atkins, Peirce, and Uyeda, all

Republicans - following Crenshaw's departure in early January 2026.

Federal law caps any single party at three seats; the two Democratic

seats remain vacant. That cap is also a leverage point: a

non-Republican commissioner, once nominated and seated, would almost

certainly dissent from an architecture this aggressive. Atkins' own

term as Chair expires in June 2026, and Peirce's commissioner term

technically expired in June 2025 (she serves on a permitted

holdover). The Commission composition that will close out this

rollout is not necessarily the Commission that started it. Comments

anchored in the architecture (third-party wrapping without issuer

consent, the "may or may not" gradient, the deliberate fragmentation

of legal-rights wrappers, the Reg NMS implications) will carry

weight that generic anti-crypto sentiment will not - and will land

in a Commission whose composition is itself in motion.

Issuer pushback matters more, not less, and the precedent exists.

The third-party wrapper design is the part of the exemption that

explicitly bypasses the issuer. The Russell 1000 CEOs whose stock is

about to be wrapped - without their consent - on crypto-native

platforms have direct standing to object. Boards have fiduciary

duties. Transfer agents have contracts. Shareholder activists have

Rule 14a-8 proposals available to put tokenization eligibility on

the annual ballot. The political cost of a handful of major issuers

refusing to acknowledge third-party wrappers as legitimate

representations of their equity would be substantial. And this is

not hypothetical: both OpenAI and Anthropic have already publicly

disavowed unauthorized tokenized products linked to their valuations

on offshore platforms. The precedent for issuer objection is

established. It needs to scale to Russell 1000 publics with active

boards and proxy seasons in front of them.

Congressional oversight - and the CLARITY Senate floor vote - is in

play. Atkins has said in public that the exemption "may require us

to explore amendments to Reg NMS." Reg NMS is the rulebook that

built the modern U.S. equity market structure. Congress has standing

to demand hearings on whether the SEC has the authority to dissolve

that architecture through staff exemption rather than statutory

rewrite. More urgently, the CLARITY Act cleared Senate Banking 15-9

on May 14, 2026, but it is not yet law. It still needs 60 votes on

the Senate floor and reconciliation between the Banking and

Agriculture versions. The two Democratic Banking votes (Gallego and

Alsobrooks) were conditional. Van Hollen's ethics amendment was

defeated 11-13 in committee but can be reintroduced on the floor.

NASAA's January 13, 2026 comment letter has already named the

architectural concern from the state-regulator side; the Warren/Van

Hollen April 27 letter named it from the Senate-minority side. A

coordinated state-regulator and Senate-minority pressure campaign on

the Senate floor schedule - using the August 2026 calendar ceiling

as the forcing function, the conditional Democratic votes as the

working surface, and a reintroduced Van Hollen amendment as the

wedge - is the single highest-leverage intervention available before

the architecture is statutorily sealed.

State law remains operative. The Uniform Commercial Code's Article 8

- which the DTC no-action letter explicitly relies on - is state

law, not federal. State legislatures in Delaware (where most public

corporations are domiciled), Texas, and Florida (which have been

actively legislating on property-rights and anti-CBDC frameworks)

can pass clarifying statutes that require any force-transfer of a

securities entitlement to occur only by court order, that prohibit

third-party tokenized wrappers from being marketed to retail

investors without explicit disclosure that the wrapper confers no

shareholder rights, or that require any tokenized representation of

a domiciled corporation's stock to obtain board consent.

Retail brokerage and platform pressure. The crypto-native rail will

live or die based on which retail platforms route order flow into

it. Direct pressure on Schwab, Robinhood, Fidelity, Vanguard, and

the rest of the working group - demanding that any third-party

wrapper offered to retail customers carry a plain-English disclosure

that the token may not confer any shareholder rights - is the

fastest market-based lever available. It does not require a single

regulator to act first.

The intellectual fight. Every line of the exemption is being drafted

by humans who answer to professional and reputational incentives.

The architectural critiques landed in Part III on the desks of the

lawyers writing the DTC request letter and the staff who issued the

no-action letter. The same critiques, sharpened by the two-rail

framing, need to land on the desks of the staff drafting the

innovation exemption - before the relief is published, not after.

The deadline I named in Part III still applies. The DTCC production

trades begin in July. The innovation exemption will be published, on

current reporting, within days. Both rails are about to move from

blueprint to live infrastructure. The window for shaping the

architecture is now measured in weeks, not months.

What I would not bet on, again, is that a parallel decentralized

system will route around all of this. The two-rail design is

engineered to absorb the offshore model, to bring xStocks-style

wrappers onshore under the SEC's seal, and to narrow the unregulated

parallel system over time rather than enlarge it. The fight is not

at the edges. It is at the center, before the center hardens.

Conclusion: One Equity, Two Cages,

No Escape Hatch

The central issue, across all four parts of this series, has not

been blockchain. It has not been crypto. It has not been efficiency,

settlement speed, or modernization. It has been whether the

architecture of ownership - and eventually of personhood - is being

rebuilt around programmable compliance, with control surfaces

concentrated in institutions that the public neither elected nor

effectively oversees.

The DTCC announcement on May 4 showed the institutional half of that

rebuild moving from concept to schedule. The innovation exemption,

now imminent, completes the rebuild by extending programmable,

permissioned, compliance-aware tokenization to the crypto-native

rail - under the SEC's seal, with third-party wrappers explicitly

authorized, with shareholder rights explicitly optional, and with

Reg NMS explicitly on the table for amendment.

That is not two competing markets. That is one architecture with two

captures: the institutional rail for regulated capital under "same

rights, same protections," and the crypto-native rail for retail and

offshore capital under "may or may not confer any rights." Both

rails permissioned. Both rails surveilled. Both rails reversible.

Both rails built on the same compliance-aware token standards. Both

rails operated, ultimately, by institutions whose root-wallet

authority is the actual source of ownership recognition.

The legal-rights gradient between the two rails is the bait. The

compliance architecture underneath both is the trap.

Once both rails are live - and they will be, within months, unless

the architecture is contested in the design space that still remains

- the question of what a share of a U.S. public company actually is

becomes a function of which rail you traded it on, which wrapper you

held it under, which protocol the issuer (or the third party) chose

to mint, and which root-key holder has the authority to reverse,

freeze, or force-transfer your position.

That is not market modernization. That is the operational rollout of

the asset layer I described in Part I, with the persona layer

described in Part II now visibly preparing to plug into both rails

of the Layer 1 that Part III documented and this essay extends.

The argument is no longer about whether tokenization is coming. It

is about whether the two-rail design is the architecture we accept -

and whether, behind every wrapper and every attestation, there

remains a human being who is real before the ledger reads them.

The rollout begins in July. The exemption lands within days. The

argument cannot wait.

References

Primary sources

-

Zennon Kapron, "America

Is About To Have Two Stock Markets For The Same Company,"

Forbes Digital Assets, May 19, 2026.

-

Bloomberg reporting (May 18, 2026),

surfaced via CoinDesk

and elsewhere, that the SEC's innovation exemption for

tokenized stocks under Project Crypto could be published

within days.

-

SEC Division of Trading and Markets,

No-Action Letter to The Depository Trust Company,

December 11, 2025 (naming ERC-3643 as a compliance-aware

protocol).

-

SEC Divisions of Corporation Finance,

Investment Management, and Trading and Markets, joint

Statement on Tokenized Securities, January 28, 2026.

-

SEC Chair Paul Atkins,

American Leadership in the Digital Finance Revolution,

speech at the America First Policy Institute, July 31, 2025

(Project Crypto, ERC-3643 the only standard named, Reg NMS

amendments).

-

Senators Elizabeth Warren and Chris Van

Hollen,

letter to Chair Atkins, April 27, 2026.

-

SEC,

Statement on Departure of Commissioner Caroline Crenshaw,

January 2026.

-

DTCC press release, "DTCC

Advances Development of New Tokenization Service, Convenes

50+ Firms to Drive Digital Assets Adoption," May 4,

2026.

-

H.R. 3633, Digital Asset Market Clarity Act of 2025,

119th Congress.

-

Senate Banking Committee,

Digital Asset Market Clarity Act section-by-section summary.

-

NASAA,

Statement of Concerns Regarding the Digital Asset Market

Clarity Act, January 13, 2026.

-

CoinDesk, "Crypto

industry cheers Senate Clarity Act markup date as market

structure push resumes," May 9, 2026.

-

Senate Banking Committee,

Chairman Scott, Senate Banking Committee Advance Clarity Act

in Historic Bipartisan Vote, May 14, 2026.

-

CoinDesk,

Clarity Act clears U.S. Senate committee, on its way to a

final test in Congress, May 14, 2026.

-

Polymarket,

Clarity Act signed into law in 2026? (market live since

January 11, 2026

Background and context

|