|

December 20, 2011 from Guardian Website

made it their business to speculate on food in 2011.

Photograph: Tim Wimborne/Reuters Last year, the price of global food floated high as ever.

That's bad news for most of us, but not for

those who trade commodities. In fact, 2011 was a great year for the traders,

who thrive on bad news, currency woes, drought, flood, freeze, fire and all

other manifestations of imminent apocalypse.

All of which meant a bumper crop for the world's

commodity exchanges - even those that used to be backwaters, like the Kansas

City Board of Trade and the Minneapolis Grain Exchange, both of which

recorded their highest electronic trading volumes in history.

Faced with a high-stakes game of price-shifting

basic ingredients, the world's largest food processors and retailers put out

the call for maths PhDs and economic modelers to theorize and implement

ever-more complex risk-management strategies just so they could keep up with

the second-by-second spikes and dips of grain and livestock futures. In the

meantime, high-frequency traders and momentum-driven hedge funds made it

their business to speculate on food.

What drove the global food market in 2011 -

other than those old faithfuls, fear and greed? I put in a call to Professor

Yaneer Bar-Yam, of the New England Complex Systems Institute (Necsi), to see

if he might have an answer.

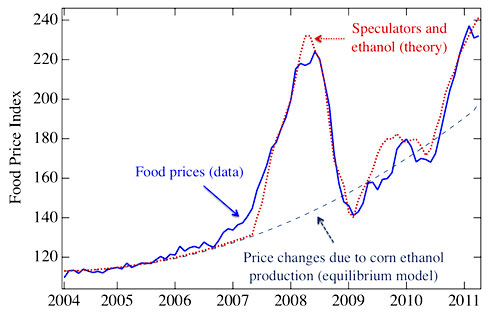

Last year, Bar-Yam and his colleagues published a paper called The Food Crises: A Quantitative Model of Food Prices Including Speculators and Ethanol Conversion, in which the Necsi crew mathematically isolated and quantified the effects of speculation as a driving force behind the bull market in global food derivatives.

According to Bar-Yam, the international thirst for biofuels has put a strain on arable land previously reserved for food production.

At the same time as the rise of the biofuel mandate, the rise of

investable commodity indexes and other electronically traded funds has

offered investors of all stripes a chance to sink their cash in a sparkling

new casino of derivative products. As a result, an ever-flowing spring of

speculative capital sustains the status quo.

In fact, Necsi's quantitative model of speculation predicted the uprisings in Tunisia, Libya and Egypt, and warned that if food prices remain inflated, riots and revolutions will go global sometime between July 2012 and August 2013.

He believes the time has come for global regulators to step in and manage the global market.

Nothing influences financial regulators like equations, so the reforms we can look forward to in 2012 will ultimately depend on the numbers.

Which is a mixed blessing.

|