by Washington's Blog

May 04, 2012

from

GlobalResearch Website

The signs are everywhere: Americans have lost

trust in our institutions.

The Chicago Booth/Kellogg School Financial Trust Index published

yesterday shows that only 22% of Americans trust the nations financial

system.

Robert Shiller

said Monday:

Our whole economy has been affected by

variations in confidence. Central banks are sort of trusted, but the

actions they have often affect peoples confidence by appearance rather

than substance. Were not in the most trusting mood now.

The National Journal

noted last week:

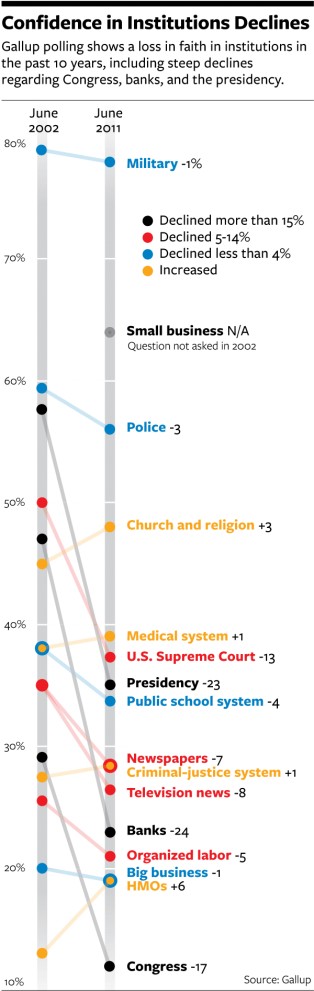

Seven in 10 Americans believe that the

country is on the wrong track; eight in 10 are dissatisfied with the way

the nation is being governed. Only 23 percent have confidence in banks,

and just 19 percent have confidence in big business.

Less than half the population expresses a

great deal of confidence in the public-school system or organized

religion. We have lost our gods, says Laura Hansen, an assistant

professor of sociology at Western New England University in Springfield,

Mass.

We lost [faith] in the media: Remember

Walter Cronkite? We lost it in our culture: You cant point to a movie

star who might inspire us, because we know too much about them. We lost

it in politics, because we know too much about politicians lives.

We've lost it that basic sense of trust and

confidence in everything.

After a 50-year decline, just 14 percent of

respondents in a 2011 Gallup Poll said that the federal government could be

trusted a great deal

Gallup reported last month that for the second year in a row Americans said

that

gold is the safest long-term investment. This shows that Americans

don't

trust the government.

Specifically, as Time Magazine

points out:

Traditionally, gold has been a store of value when citizens do not trust

their government politically or economically.

Indeed:

-

A tiny percent of Americans believe that

the U.S. government

has the consent of the governed

-

A higher percentage of Americans

believed in King George of England during the Revolutionary War than

believe in congress today

-

Many Americans

disbelieve the

government's rosy statements about the economy

-

An NBC News/Wall Street Journal poll

from November found that 76% of Americans believe that the country's

current financial and political structures

favor the rich over the

rest of the country

-

The U.S. financial system is so corrupt

and unregulated that many don't believe the government and

businesses promises to follow the rule of law and simply

won't do

business here anymore

Its not just the U.S.

As the Economist reported in January, trust in institutions is

plunging

worldwide:

The latest annual trust barometer published

by Edelman, a PR firm, on January 24th [finds that] overall trust has

declined in the leaders of the four main categories of organization

scrutinized government, business, non-governmental organizations and the

media.

Of the 50 or so countries examined, 11,

nearly twice as many as last year, are now judged skeptical, with less

than 50% of those polled saying they trusted these institutions. Trust

in Japanese institutions plunged to 34%, from 51% in 2011, not

surprising given the handling by leaders of the Tsunami and its

aftermath.

But the collapse in trust was even more

striking in Brazil, the country in which trust was greatest in 2011, at

80%, but now, following a series of corruption scandals, has slipped to

51% (admittedly, still above America and Britain, among others).

This headline slump in trust is due, above all,

to the public losing faith in political leaders.

In 2011, across all countries, Edelman found

that 52% of those polled trusted government; this year, it was only 43%.

Government is now trusted less even than the media. Trust in business fell

slightly, from 56% to 53%, as did trust in NGOs, which still remain the most

trusted type of institution, at 58%, down from 61% in 2011.

As in previous years, the barometer is based on

a poll of what Edelman calls informed people, which typically means

professional and well-educated, though this year for the first time the

views of the informed were benchmarked against a poll of the public as a

whole.

For each institution, the broader public was

even less trusting than the informed, with government trusted by 38%,

business 47%, NGOs 50% and the media 46%.

Lack of Trust Is

Killing the Economy

Top economists have been saying for well over a decade that trust is

necessary for a stable economy, and that prosecuting the criminals is

necessary to restore trust.

Indeed, as we have

repeatedly noted, loss of

trust is arguably the main reason we are

stuck in an economic crisis

notwithstanding

unprecedented action by central banks worldwide.

Economist Daniel Hameresh writes:

A number of economists have shown recently

that income levels and real growth depend upon trust greases the wheels

of exchange.

In 1998, Paul Zak (Professor of Economics

and Department Chair, as well as the founding Director of the Center for

Neuroeconomics Studies at Claremont Graduate University, Professor of

Neurology at Loma Linda University Medical Center, and a senior researcher

at UCLA) and Stephen Knack (a Lead Economist in the World Banks

Research Department and Public Sector Governance Department)

wrote a paper

called

Trust and Growth, arguing:

Adam Smith observed notable differences

across nations in the probity and punctuality of their populations. For

example, the Dutch are the most faithful to their word.

John Stuart Mill wrote: There are countries

in Europe... where the most serious impediment to conducting business

concerns on a large scale, is the rarity of persons who are supposed fit

to be trusted with the receipt and expenditure of large sums of money

(Mill, 1848, p. 132).

Enormous differences across countries in the

propensity to trust others survive today.

-

Trust is higher in fair societies.

-

High trust societies produce more output

than low trust societies. A fortiori, a sufficient amount of trust

may be crucial to successful development. Douglass North (1990, p.

54) writes,

-

If trust is too low in a society,

savings will be insufficient to sustain positive output growth. Such

a poverty trap is more likely when institutions - both formal and

informal which punish cheaters are weak.

Heap, Tan and Zizzo and others have come to

similar conclusions.

In 2001, Zak and Knack

showed that strengthening the rule of law, reducing

inequality, and by facilitating interpersonal understanding all increase

trust. They conclude:

Our analysis shows that trust can be raised

directly by increasing communication and education, and indirectly by

strengthening formal institutions that enforce contracts and by reducing

income inequality.

Among the policies that impact these

factors, only education, and freedom satisfy the efficiency criterion

which compares the cost of policies with the benefits citizens receive

in terms of higher living standards. Further, our analysis suggests that

good policy initiates a virtuous circle: policies that raise trust

efficiently, improve living standards, raise civil liberties, enhance

institutions, and reduce corruption, further raising trust.

Trust, democracy, and the rule of law are

thus the foundation of abiding prosperity.

A 2005 letter in premier scientific journal

Nature

reviewed the research on trust and economics:

Trust plays a key role in economic

exchange and politics. In the absence of trust among trading partners,

market transactions break down. In the absence of trust in a country's

institutions and leaders, political legitimacy breaks down. Much recent

evidence indicates that trust contributes to economic, political and

social success.

Forbes wrote an article in 2006 entitled

The

Economics of Trust.

The article summarizes the importance of trust in

creating a healthy economy:

Imagine going to the corner store to buy a

carton of milk, only to find that the refrigerator is locked. When

you've persuaded the shopkeeper to retrieve the milk, you then end up

arguing over whether you're going to hand the money over first, or

whether he is going to hand over the milk.

Finally you manage to arrange

an elaborate simultaneous exchange. A little taste of life in a world

without trust now imagine trying to arrange a mortgage.

Being able to trust people might seem like a

pleasant luxury, but economists are starting to believe that its rather more

important than that.

Trust is about more than whether you can leave your

house unlocked; it is responsible for the difference between the richest

countries and the poorest.

If you take a broad enough definition of trust, then it would explain

basically all the difference between the per capita income of the United

States and Somalia, ventures Steve Knack, a senior economist at the World

Bank who has been studying the economics of trust for over a decade.

That suggests that trust is worth $12.4 trillion

dollars a year to the U.S., which, in case you are wondering, is 99.5% of

this country's income.

Above all, trust enables people to do

business with each other. Doing business is what creates wealth.

Economists distinguish between the personal,

informal trust that comes from being friendly with your neighbors and the

impersonal, institutionalized trust that lets you give your credit card

number out over the Internet.

In 2007, Yann Algan (Professor of Economics at Paris School of

Economics and University Paris East) and Pierre Cahuc (Professor of

Economics at the Ecole Polytechnique - Paris)

reported:

We find a significant impact of trust on

income per capita for 30 countries over the period 1949-2003.

Similarly, market psychologists Richard L.

Peterson M.D. and Frank Murtha, PhD

noted in 2008:

Trust is the oil in the engine of

capitalism, without it, the engine seizes up. Confidence is like the

gasoline, without it the machine wont move.

Trust is gone: there is no longer trust

between counterparties in the financial system. Furthermore, confidence

is at a low. Investors have lost their confidence in the ability of

shares to provide decent returns (since they haven't).

In 2009, Paola Sapienza (associate

professor of finance and the Zell Center Faculty Fellow at Northwestern

University) and Luigi Zingales (Robert C. McCormack Professor of

Entrepreneurship and Finance at the University of Chicago Booth School of

Business)

pointed out:

The drop in trust, we believe, is a major

factor behind the deteriorating economic conditions.

As trust declines, so does Americans willingness

to invest their money in the financial system.

Our data show that trust in the stock market

affects peoples intention to buy stocks, even after accounting for

expectations of future stock-market performance. Similarly, a persons trust

in banks predicts the likelihood that he will make a run on his bank in a

moment of crisis: 25 percent of those who don't trust banks withdrew their

deposits and stored them as cash last fall, compared with only 3 percent of

those who said they still trusted the banks.

Thus, trust in financial institutions is a key

factor for the smooth functioning of capital markets and, by extension, the

economy. Changes in trust matter.

They quote a Nobel laureate economist on the subject:

Virtually every commercial transaction has

within itself an element of trust, writes economist Kenneth Arrow, a

Nobel laureate. When we deposit money in a bank, we trust that its safe.

When a company orders goods, it trusts its counterpart to deliver them

in good faith. Trust facilitates transactions because it saves the costs

of monitoring and screening; it is an essential lubricant that greases

the wheels of the economic system.

In 2010, a distinguished international group of

economists (Giancarlo Corsetti, Michael P. Devereux, Luigi Guiso, John

Hassler, Gilles Saint-Paul, Hans-Werner Sinn, Jan-Egbert Sturm and Xavier

Vives)

wrote:

Public distrust of bankers and financial

markets has risen dramatically with the financial crisis. This column

argues that this loss of trust in the financial system played a critical

role in the collapse of economic activity that followed. To undo the

damage, financial regulation needs to focus on restoring that trust.

They noted:

Trust is crucial in many transactions and

certainly in those involving financial exchanges. The massive drop in

trust associated with this crisis will therefore have important

implications for the future of financial markets. Data show that in the

late 1970s, the percentage of people who reported having full trust in

banks, brokers, mutual funds or the stock market was around 40%; it had

sunk to around 30% just before the crisis hit, and collapsed to barely

5% afterwards. It is now even lower than the trust people have in other

people (randomly selected of course).

In his influential 1993 book Making Democracy

Work, Robert Putnam

showed how civic attitudes and trust could account for

differences in the economic and government performance between northern and

southern Italy.

Political economist Francis Fukiyama wrote a book called

Trust in

1995, arguing that the most pervasive cultural characteristic influencing a

nations prosperity and ability to compete is the level of trust or

cooperative behavior based upon shared norms.

He stated that the United

States, like Japan and Germany, has been a high-trust society historically

but that this status has eroded in recent years.

Chris Farrell

notes:

Trust matters. Its kind of like a recipe or

a software protocol that allows for economic exchange and all kinds of

innovation.

There's compelling evidence that both higher

levels of trust in institutions and a belief in the general trustworthiness

of individuals in society carry large economic benefits. Sociologists,

political scientists and economists have all showed in an impressive body of

research that higher levels of trust increase trade and even foster economic

growth.

Dallas Fed president Richard Fisher

said last year that a growing

distrust of the nations political institutions is keeping businesses on the

sidelines.

Forbes notes in March that a lack of trust was

one of the main factors

hurting the Greek economy:

There are a number of issues that have

contributed and exacerbated the levels of distrust. For instance,

Greece, with the help of Goldman Sachs,

concealed the state of their

finances for over a decade until they ran into this major debt crisis.

Because they failed to disclose the extent of their financial problems,

the EU and other players in the global credit market are extremely

reluctant to cooperate or put faith in the representations made by the

Greek leadership.

If the leadership in Athens cannot reestablish

trust with the citizenry and develop open and honest communication amongst

themselves, their constituents, and the individual leaders of the financial

institutions involved, the agreements they make will not even be worth the

paper they are written on.

Ken Eisold - an internationally respected authority on the

psychodynamics of organizations -

writes:

Most of us view trust as valuable and

desirable, something that improves the quality of our personal lives. We

seldom take the next step and view it as indispensable, a vital

ingredient in society and in the economy. But all credit is based on

trust, and the fundamental problem in a credit crisis is not just the

lack of liquidity but also the absence of trust, the trust that is

essential to all financial transactions.

But the problem is not that people should be

more blindly and naively trusting.

The problem as Eisold points out is that the

institutions have to act in a more trustworthy manner:

The essential point is not that people need

to be encouraged to trust. Most of us want to trust and have the basic

capacity to trust. We need institutions that are trustworthy.

No Economy-Revving

Optimism Without Trust

Economist Robert Higgs who has studied the effect of World War II on

the economy in great detail argues that it was optimism, rather than

stimulus spending, which

got us out of the depression:

The performance of the war economy broke the

back of the pessimistic expectations almost everybody had come to hold

during the seemingly endless Depression. In the long decade of the

1930s, especially its latter half, many people had come to believe that

the economic machine was irreparably broken.

The frenetic activity of war production

never mind that it was just a lot of guns and ammunition dispelled the

hopelessness. People began to think: if we can produce all these planes,

ships, and bombs, we can also turn out prodigious quantities of cars and

refrigerators.

The transformation of expectations justify an

interpretation that views the war as an event that recreated the possibility

of genuine economic recovery. As the war ended, real prosperity returned.

Unlike after WWII, Americans now are pessimistic (even though we've been

various wars against third-rate countries far longer than we were in WWII)

and our expectations are stuck in the gutter.

Why?

Perhaps because we don't trust our government, our big corporations or our

other institutions to do anything very helpful for the country. Indeed, we

don't trust our government, big corporations and other institutions to even

allow a fair playing field where we have a chance of competing fairly to get

ahead on our own initiative.

Why should we work harder, invest more or spend more when we don't trust

that we might have a bright future?

Prosecuting the

Criminals Is Necessary to Restore Trust

Nobel prize winning economist Joseph Stiglitz says that we

have to

prosecute fraud or else the economy wont recover:

The legal system is supposed to be the

codification of our norms and beliefs, things that we need to make our

system work. If the legal system is seen as exploitative, then

confidence in our whole system starts eroding. And that's really the

problem that's going on.

I think we ought to go do what we did in the

S&L [crisis] and actually put many of these guys in prison. Absolutely.

These are not just white-collar crimes or little accidents. There were

victims. That's the point. There were victims all over the world.

Economists focus on the whole notion of

incentives.

People have an incentive sometimes to behave

badly, because they can make more money if they can cheat. If our economic

system is going to work then we have to make sure that what they gain when

they cheat is offset by a system of penalties.

Robert Shiller

said recently that failing to address the legal issues

will cause Americans to lose faith in business and the government:

Shiller said the danger of foreclosure gate

the scandal in which it has come to light that the biggest banks have

routinely mishandled homeownership documents, putting the legality of

foreclosures and related sales in doubt is a replay of the 1930s, when

Americans lost faith that institutions such as business and government

were dealing fairly.

Economists such as William Black and

James

Galbraith agree.

Galbraith

says:

There will have to be full-scale

investigation and cleaning up of the residue of that, before you can

have, I think, a return of confidence in the financial sector. And

that's a process which needs to get underway.

Galbraith

also says that economists should move

into the background, and criminologists to the forefront. Government

regulators know this or at least pay lip service to it as well.

For example, as the Director of the Securities

and Exchange Commissions enforcement division

told Congress:

Recovery from the fallout of the financial

crisis requires important efforts on various fronts, and vigorous

enforcement is an essential component, as aggressive and even-handed

enforcement will meet the publics fair expectation that those whose

violations of the law caused severe loss and hardship will be held

accountable.

And vigorous law enforcement efforts will

help vindicate the principles that are fundamental to the fair and

proper functioning of our markets: that no one should have an unjust

advantage in our markets; that investors have a right to disclosure that

complies with the federal securities laws; and that there is a level

playing field for all investors.

Nobel prize winning economist George Akerlof

has demonstrated that failure to punish white collar criminals and instead

bailing them out- creates incentives for more economic crimes and further

destruction of the economy in the future.

Indeed, William Black

notes that

we've known of this dynamic for hundreds of years. And see

this,

this,

this and

this.

And when Zak and Knack quoted above discuss enforcing contracts, raising

civil liberties, and reducing corruption, they are talking about enforcing

the rule of law, which means prosecuting violations of the law. Likewise,

when they refer to enhancing institutions, they mean regulatory and justice

systems which enforce contracts and prosecute cheaters.

And when Zak

and Knack promote reduction of inequality, that means prosecuting fraud as

well. Specifically, as I recently

pointed out, prosecuting fraud is the best

way to reduce inequality:

Robert Shiller [one of the top housing economists in the United

States]

said in 2009:

And its not like we want to level income.

I'm not saying spread the wealth around, which got Obama in trouble. But

I think, I would hope that this would be a time for a national

consideration about policies that would focus on restraining any

possible further increases in inequality.

If we stop bailing out the fraudsters and

financial gamblers, the big banks would

focus more on traditional lending

and less on speculative plays which only make the rich richer and the poor

poorer, and which guarantee future economic crises (which hurt the poor more

than the rich).

Moreover, both conservatives and liberals agree that we need to prosecute

financial fraud. As I've

previously noted, fraud disproportionally benefits

the big players, makes boom-bust cycles more severe, and otherwise harms the

economy all of which increase inequality and warp the market.

Of course, its not just economists saying this.

One of the leading business schools in America - the Wharton School of

Business -

published an essay by a psychologist on the causes and solutions to

the economic crisis.

Wharton points out that restoring trust is the

key to recovery, and that trust cannot be restored until wrongdoers are held

accountable:

According to David M. Sachs, a training and

supervision analyst at the Psychoanalytic Center of Philadelphia, the

crisis today is not one of confidence, but one of trust.

Abusive financial practices were unchecked

by personal moral controls that prohibit individual criminal behavior,

as in the case of [Bernard] Madoff, and by complex financial

manipulations, as in the case of AIG.

The public, expecting to be protected from

such abuse, has suffered a trauma of loss similar to that after 9/11.

Normal expectations of what is safe and dependable were abruptly

shattered, Sachs noted. As is typical of post-traumatic states, planning

for the future could not be based on old assumptions about what is safe

and what is dangerous.

A radical reversal of how to be gratified

occurred.

People now feel more gratified saving money than

spending it, Sachs suggested.

They have trouble trusting promises from the

government because they feel the government has let them down.

He framed his argument with a fictional patient named Betty Q. Public, a

librarian with two teenage children and a husband, John, who had recently

lost his job. She felt betrayed because she and her husband had invested

conservatively and were double-crossed by dishonest, greedy businessmen, and

now she distrusted the government that had failed to protect them from

corporate dishonesty.

Not only that, but she had little trust in

things turning around soon enough to enable her and her husband to

accomplish their previous goals.

By no means a sophisticated economist, she knew that some people had

become fantastically wealthy by misusing other peoples money hers included,

Sachs said. In short, John and Betty had done everything right and were

being punished, while the dishonest people were going unpunished.

Helping an individual recover from a traumatic experience provides a useful

analogy for understanding how to help the economy recover from its own

traumatic experience, Sachs pointed out.

The public will need to hold the perpetrators of

the economic disaster responsible and take what actions they can to prevent

them from harming the economy again. In addition, the public will have to

see proof that government and business leaders can behave responsibly before

they will trust them again, he argued.

Note that Sachs urges hold[ing] the perpetrators of the economic disaster

responsible. In other words, just looking forward and promising to do things

differently isn't enough.

As Wall Street insider and New York Times columnist Andrew Ross Sorkin

writes:

"They will pick on minor misdemeanors by

individual market participants, said David Einhorn, the hedge fund

manager who was among the Cassandras before the financial crisis. To Mr.

Einhorn, the government is not willing to take on significant

misbehavior by sizable firms.

But since there have been almost no big

prosecutions, there's very little evidence that it has stopped bad

actors from behaving badly."

Fraud at big corporations surely dwarfs by

orders of magnitude the shareholders losses of $8 billion that Mr. Holder

highlighted

If the government spent half the time trying to

ferret out fraud at major companies that it does tracking pump-and-dump

schemes, we might have been able to stop the financial crisis, or at least

wed have a fighting chance at stopping the next one.

Of course, the Europeans have been trying to

avoid fraud prosecutions as

well.

On the other hand, Iceland has prosecuted the

fraudster bank heads (and

here and

here) and their former prime minister, and their economy is

recovering

nicely because trust is being restored in the financial system.

Indeed, even evangelical leader Pat Robertson

agrees:

Pat Robertson discussed the banking crisis

and glowingly spoke about how Iceland jailed many of the bankers who

devastated their nations economy by taking out fraudulent loans.

Robertson hailed the Nordic nation for its actions and said that

Americans should deal with the financial crisis in the same way.

They are putting people in jail.

Prime ministers are being indicted. They are

going after banks. The people said the banks are ripping us off. We don't

like what they did, and they brought our country to ruin. Suddenly, Iceland

is turning around and they look like a big success story!

We could start putting all of those bankers in jail. There was not one

banker prosecuted and so many people were lying, and so-called no-doc loans

and liars loans, and none of them have been held accountable.

Iceland is leading the way and their GDP is growing, and all of a sudden,

they were in a terrible mess, terrible mess, and look what is happening!