|

by Scott S. Bateman

July 21,

2018

from

Medium Website

|

Scott S. Bateman is a journalist and entrepreneur. He

spent 20 years in senior and middle management at two

major media companies.

https://www.PromiseMedia.com

|

Credit: Pixabay

Creative Commons license

The death of

the newspaper industry is a

legend-in-the-making story about managers who oppose change.

It's also a lesson in how

to undermine innovation...

Business schools and business books often cite the

collapse of Eastman Kodak as a leading example of what happens

to companies when their managers refuse to innovate.

Kodak dominated print

photography for decades and fought against the transition to digital

until too late.

"More than 130 years

after a 'not especially gifted' high school dropout, George

Eastman, founded the camera company that dominated photography

for most of the 20th century, Eastman Kodak filed for

bankruptcy protection in the U.S. on Thursday," The Guardian

newspaper said on Jan. 19, 2012.

Part of the company

eventually came out of bankruptcy and focuses today on a much

smaller market:

business imaging.

The Kodak failure is

minor compared to the state of the newspaper industry. Print

newspapers are quickly shrinking staffs, budgets and product sizes

even during a growing economy.

Although some seem to have a future online - the New York Times

is a notable example - the print versions will cease to exist at

some point in the near future.

Their costly newsprint,

printing plants and manual circulation systems are too expensive to

compete with digital publishing that has none of these costs.

Like Kodak, newspapers waited until too late to innovate

aggressively and prepare for the massive changes resulting from the

digital distribution of information.

Newspapers closed or

suffered layoffs at an alarming rate during the

2008 Great Recession and will do so

again during the next recession.

The (Denver) Post has

cut its staff about 70 percent since Alden and its founder

Randall Smith took control in 2011, according to data from the

Denver Newspaper Guild.

CNBC, June 16, 2018

How did an industry with

near monopoly status in local markets get to this point?

They did it in 10 ways

involving slow innovation, no innovation or resistance to it.

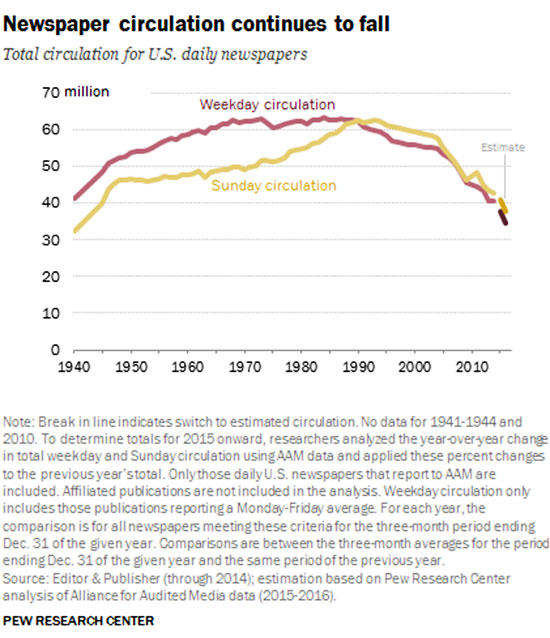

1 - They saw

digital as a threat

Digital wasn't just a threat to the print business.

It was a personal threat

to the compensation of executives, senior managers and middle

managers.

Credit: Pew Research Center

Newspapers often use management by objectives in their compensations

models.

Pay raises, bonuses and

commissions depend on achieving targets for advertising sales and

circulation subscriptions. Editors saw the threat as an attack on

their readership.

Newspaper websites pulled

readers and advertisers away from the print product. Even worse,

managers received little or no compensation tied to digital

performance.

Innovation requires a willingness to take risks even at the

potential expense of the core business.

It shouldn't come at a

cost to the compensation of managers and employees.

2 - They

jammed a print business model into an online environment

Publishers and circulation managers in particular believed that

newspaper websites should require paid subscriptions in the same way

that most newspapers require them.

From the beginning, they made repeated attempts to make people pay

for access.

Nearly all of them

failed, but they continued to spend money, use valuable time and

energy, and chase away website visitors with more attempts.

Free TV station websites

gained customers as a result.

One exception was the New York Times, which made a

substantial investment in new content for a paid online product that

went far beyond the daily print version.

"Digital-only

subscriptions totaled approximately 2,644,000 at the end of the

fourth quarter of 2017, a net increase of 157,000 subscriptions

compared with the end of the third quarter of 2017 and a 41.8

percent increase compared with the end of the fourth quarter of

2016."

The

New York Times

Publishers didn't

understand that people could now get local news, sports results,

weather forecasts and other information from free websites produced

by TV stations, other businesses and a wide variety of nonprofits,

schools and government agencies.

Innovation thrives in part because of creative thinking and a new

way of looking at a business.

It doesn't thrive with

restrictions from old and sometimes outdated rules.

The cost structure of print newspapers

can't

compete with more efficient digital publishing.

Credit:

Pixabay Creative Commons license

3 - They

didn't understand they lost their monopoly status

Newspapers in recent decades largely had a monopoly status in the

cities and towns where they were located.

As a result, they had

exceptional reach and control over readership and advertising.

During the 1990s, rising national websites offered much of the same

information newspapers had traditionally offered such as TV

programming, stock quotes, national and international news, national

sports news, cartoons, recipes, columnists and movie reviews.

Those sections in

newspapers shrank or even vanished in response.

Even more painfully came the competitors to advertising, especially

the highly lucrative classified ad categories of,

-

employment

(Indeed and Monster)

-

automotive (AutoTrader,

Cars.com and many more)

-

real estate (Zillow

and Realtor.com)

In response, many

newspaper companies tried to protect their employment advertising

business and instead destroyed it by partnering with the now-defunct

Yahoo! HotJobs.

Local innovators learned how to publish their own local news,

weather and sports.

The above mentioned

nonprofits, schools and government agencies built websites that had

much more information than newspapers could offer in print because

of space limitations. No such limitations exist on a website.

Successful innovation is a timely, proactive response to a change in

the business environment.

It requires an open mind

and careful observation of trends in the community and industry.

4 - They

undermined their own innovators

Many entrepreneurs within major newspapers were required to follow

harsh rules that undermined their own profitability.

One newspaper company required its own website operation to pay $1

million a year for the right to publish the newspaper's content. The

same newspaper was making a small fraction of that amount by selling

it to other electronic services such as LexisNexis.

Exorbitant fees prevented profitability, which in turn raised

accusations that newspaper websites weren't financially viable.

The lack of

"profitability" also undercut future growth and critical investments

in content and staff. Internal jealousy and opposition blocks

innovation.

Executive management has

a responsibility to remedy the causes of any opposition.

If necessary, those

remedies include firing or demoting managers who stand in the way of

innovation.

5 - They

either over invested or under invested online

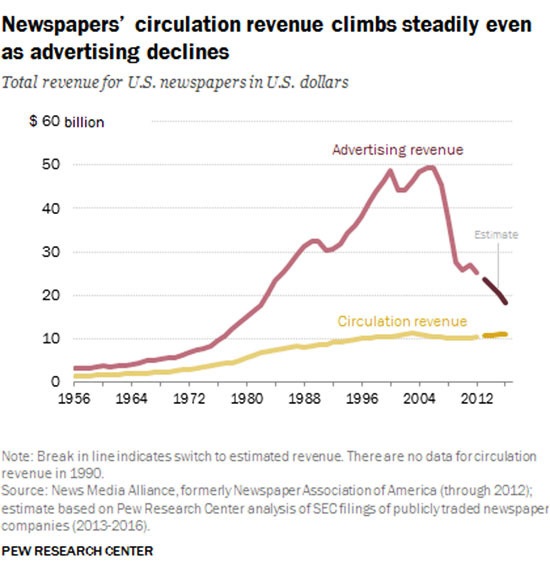

Credit: Pew Research Center

Some newspaper companies did make major investments in online

operations during the early years of web browsing.

But the investments were

so large that the financial losses resulted in massive pullbacks and

staff layoffs.

In their case, they invested too early in online before online

advertising revenue had risen enough. The financial scars made them

reluctant about future large investments.

When the 20018 Great

Recession hit, they could no longer afford big investments at all.

Managers who are given the responsibility for innovating a new

product, service, division or even company need constant vigilance

over the rate and timing of investments.

6 - They got

addicted to 40 percent profit margins

Astonishingly, some newspapers achieved profit margins as high as 40

percent as a result of having a local monopoly.

It was a drug too good to

give up...

As print margins started declining, these same newspapers opposed

online investments in order to protect the print profit. It was a

fixation on short term solutions to smaller problems at the expense

of much bigger problems in the years ahead.

Few print newspapers if any now enjoy 40 percent profit margins.

As a result, low margins

inhibit innovation because of the potential risk of failure and

unacceptable costs.

"The Richmond

Times-Dispatch on Monday laid off 33 full-time employees and

announced a reorganization of the printed newspaper as a result

of declines in print revenue."

The

Times-Dispatch, April 3, 2017

7 - They got

lazy

Google and executives at other

online companies were famously known for working more than 100 hours

a week to build their high-growth companies.

Likewise, those same

companies had lucrative compensation packages for people in middle

management to encourage their own exceptional workload and a

constant focus on innovation.

Anecdotally, I didn't know any newspaper executives who regularly

worked those kind of hours during a lifetime in the industry.

I certainly didn't know

any managers in the lower ranks who worked more than 50–55 hours a

week on a regular basis because they weren't paid to work that way.

Besides, the high profit

margins needed protecting.

No newspaper executive or senior manager will ever admit to being

lazy, which is a harsh and relative term. Some like myself did have

temporary spikes in their hours, especially during budget time.

But it's true that they

simply were outworked by the competition.

"The other piece that

gets overlooked in the Google story is the value of hard work.

When reporters write

about Google, they write about it as if it was inevitable. The

actual experience was more like, 'Could you work 130 hours in a

week'?" said Marissa Mayer, former Yahoo! CEO and one of the

first Google employees.

"The answer is yes, if you're strategic about when you sleep,

when you shower, and how often you go to the bathroom. The nap

rooms at Google were there because it was safer to stay in the

office than walk to your car at 3 a.m.

For my first five

years, I did at least one all-nighter a week, except when I was

on vacation - and the vacations were few and far between."

8 -

Executives paid themselves first

As a fairly successful small business owner after leaving senior

management, I learned the survival of my newspaper consulting

business came first and my personal financial desires came second.

I pocketed the smallest

amount of monthly compensation possible and waited until the end of

every year either to take profit out of the business or reinvest the

profit into it.

Even during the depths of the recession, some newspaper companies

increased their executive compensation despite plunging profits.

They also gave away zero-based stock options that diluted their

stock equity.

(A zero-based option is

the right to buy company stock without having to pay for it, then

sell it on the market at full price.)

In the meantime, many of these executives laid off employees,

stopped salary increases, killed pensions and ended matching

contributions for 401k plans.

Demotivating employees

while increasing executive compensation is not a way to protect the

business or encourage innovation.

9 - They

took on too much debt

Some newspaper owners recognized the severity of the trends and sold

their companies.

Examples include the

Pulitzer family and the Graham family of the Washington Post.

Other owners went in the opposite direction. They bought the media

properties including newspapers and TV stations that went up for

sale before the Great Recession.

Remarkably, they bought

these properties even as their own numbers were declining.

When the Great Recession hit, a combination of their debt payments

and plunging profits made it more difficult than ever to innovate.

Some declared bankruptcy; others will declare it during the next

recession.

Aggressive innovation is possible with strong financials.

Google couldn't afford

the $571 million loss during the first quarter of 2018 in its

Other Bets subsidiary without the company's 22 percent net

profit margin.

10 - They

ignored new online streams of revenue

Newspaper executives think of two critical business metrics for

print:

They provide nearly all

of the revenue that has made newspapers so profitable over decades

and even centuries.

But the same isn't quite true about online publishing because

competition decreases the potential revenue from readers and

advertisers. Some newspaper publishers understood that point.

They tried to diversify

into other revenue streams such as website hosting and design and

even selling the products of competitors such as

Google AdWords.

Many publishers became so captivated by trying to defend plunging

profit margins that they had no time, money or staff to pursue other

streams of revenue with enough success.

Newspapers as we have known them are going through historic changes

that showcase the impact of innovation at a societal level on an

entire industry.

It also showcases what

happens when the industry struggles with its own innovation in

response.

|